This event has now taken place but you can watch the video recording of it through our Youtube Channel, get to it by clicking the button below

When

Tuesday, August 8th 2023 from 6pm - 7:30pm BSTWhere

Online via Zoom.Format

There'll be a great line-up of speakers plus ample scope for discussion and debate.Why You Should Attend...

As you may already know the collective endeavour campaign to ask the Treasury Committee to open an inquiry on SME Finance and the Business Banking Resolution Service (BBRS) has been a success – the inquiry we all asked for has been opened.

We are extremely grateful that the Treasury Committee has opened it. Here’s Chair Harriett Baldwin MP’s comment:

“Small businesses are the lifeblood of local communities, powering economic growth and fostering innovation and an entrepreneurial spirit.

As a Committee, we’ll be examining whether small businesses are able to access the finance they need to grow and develop, whether there is adequate regulation of the sector, and if Government can take a more active role to support business growth.

We look forward to receiving written evidence on this important topic and taking oral evidence later in the year.”

Here’s the official announcement.

We now urge anybody that has been a victim of banking misconduct, especially those that have had an unpleasant experience/outcome of dealing with the Business Banking Resolution Service (BBRS), to respond to the consultation.

Full details about the consultation are here and note the deadline is now Friday 1st September (it has been pushed back from 13th August).

Please note that the consultation covers many topics, TTF’s response is going to focus mostly (but not only) on this part:

- How effective has the Business Banking Resolution Service been, and what lessons can be learnt from it?

Given the importance that we collectively respond to this consultation as impactful as possible, it is vital that as many submissions are made as can be organised.

Please do make a submission yourselves; be that in an individual or organisational capacity.

TTF will of course be responding and we are busy putting together our response.

We have organised this special Zoom meeting taking place on 8th August to:

- Talk about our proposed response, which should be in first draft by then

- Absorb ideas that attendees want to share that we should consider including before we finalise our response

- Make sure everybody knows the range of topics that we plan to include in our response, so if anybody wants to make use of our ideas in their own response they can.

Please do be sure to attend the event if you have been a victim of any kind of banking misconduct, especially if you have dealt with the BBRS.

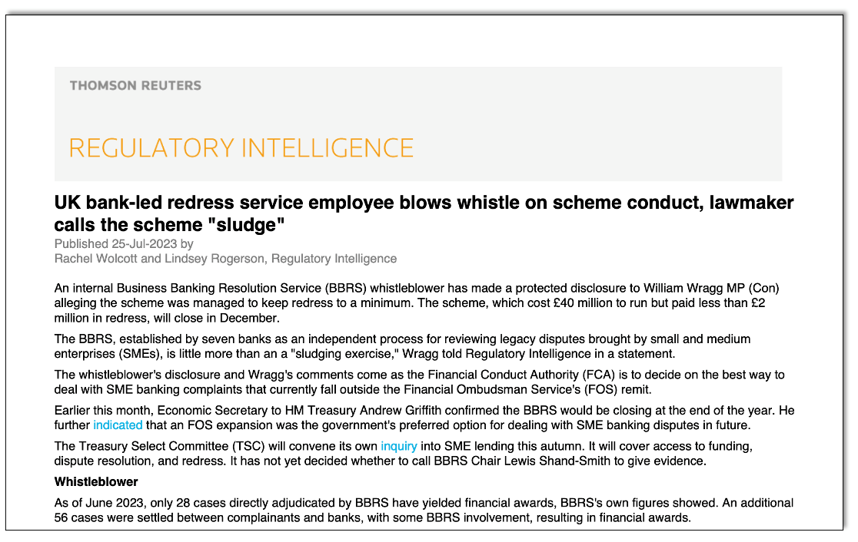

We are continuing to discover more and more about the shortcomings of the BBRS, and it’s important to know that a whistleblower has now stepped forward who has bravely shared insights into what’s really been going on within BBRS.

We urge you to read the first class article written by Rachel Wolcott and Lindsey Rogerson, Regulatory Intelligence Reporters at Thomson Reuters, see below

You can access the article in full here.

As we see it so far (noting that we are still learning more about the BBRS’ shortcomings), there are 5 major problems that the BBRS has:

- The Independence Problem: The badly compromised governance structure of the BBRS means the directors are not truly independent. That’s a problem because the BBRS was sold to stakeholders as being independent. The participating banks fund it, and as the saying goes “he who pays the piper calls the tune”. The banks also get to “mark their own homework”. So we have a rather bizarre situation where the banks are the judge, jury and proven perpetrator, and as such we feel totally justified in referring to the BBRS’s governance structure as ‘badly compromised’.

The participating banks created a company, known as the Bank Appointed Member. It is jointly owned by them and it has the power to block the directors from exercising key powers they would normally be expected to hold. See page nine and the final page of the Articles of Association, here. The BBRS’ supposedly independent leadership team is disinclined to push through change without the approval of the Bank Appointed Member. Furthermore, there are also concerns about the independence of some of the adjudicators because they include former bank employees who sold Interest Rate Hedging Products, which are the basis of many victims’ claims. Are they not therefore obviously conflicted and anything but independent?

- The Eligibility Criteria Problem: The lack of independence of the BBRS has led to the Scheme’s Eligibility Criteria being unduly limited, resulting in almost all prospective claims being excluded. UK Finance is reluctant to change the criteria and there is disagreement about whether the Scheme rules are being interpreted correctly. That’s a problem because the extremely low number of cases that have been resolved means the BBRS has not achieved its central purpose – to resolve a meaningful number of cases. When the BBRS was being established, UK Finance estimated that some 60,000 firms would be within scope for the historical scheme, which in theory deals with legacy misconduct cases such as RBS GRG, HBoS Reading, IRHP mis-selling, Lloyds BSU cases, bank signature forgery cases and more. In fact, with that legacy scheme having been closed to new applications on 14th February 2023, the number of cases resulting in financial awards at the time of writing is currently just 18.

- The Trust and Confidence Problem: Trust and confidence between the banks and business has not been restored; if anything it has been worsened. That’s a problem because rebuilding trust and confidence was a central purpose of the BBRS, as expressed by then-Chancellor Philip Hammond. Some believe that the BBRS started off as an authentic, genuine endeavour by the banks to tidy up the many and extensive messes they created and for them to be rehabilitated i.e. to change their ways from the exploitative, predatory, dishonest, devious and profit-regardless-of-the consequences-and-the-carnage-caused entities that they were.

But others believe the BBRS was never a genuine, authentic effort by the banks. Rather, that it has been something of a “rehabilitation smokescreen” designed to make it look like a fair mechanism had been put in place for businesses to get the compensation they deserved and that the banks were willing and able to undertake a “cultural transfusion” from the exploitative and predatory organisations they were to something honest and ethical.

- The Consequential Reputational Damage Problem: The abysmal failure of the BBRS to deliver on its purpose is continuing to cause reputational damage to the Government (particularly HM Treasury) and also to the Financial Conduct Authority which is meant to ensure good conduct by the banks. That’s a problem because the Government, HM Treasury and the Financial Conduct Authority are meant to be in charge. The very public ongoing failure of the BBRS is happening on their watch, so it’s not a good look for them that the banks through UK Finance and the BBRS seem to be in the driving seat. Isn’t this a classic case of “the tail wagging the dog?”

- The Opportunity Cost Problem: Four years and a great deal of money have been largely wasted getting to this point with the BBRS. That’s a problem because in the meantime there has been ongoing suffering for thousands of victims of banking fraud and misconduct. In hindsight, it is now crystal clear that the idea of a statutory tribunals framework would have been a far better approach. Since the BBRS experiment has been tried but failed, the intervention of the Government is now needed to create a route to justice, through a statutory tribunals framework.

These are the headings that we have so far in our submission:

- Background to the BBRS

- The establishment of the BBRS

- Persistent reasons for concern

- Expectations about the BBRS set by The Chancellor of the Exchequer

- Expectations set by other stakeholders

- What was the role of law firm Osborne Clarke?

- The Discovery of the Bank Appointed Member (BAM)

- Is the Bank Appointed Member a Person of Significant Control?

- Is the BBRS a distinct enterprise?

- Was the FCA correct to subcontract to the BBRS in the first place?

- What has the BBRS spent?

- What has the BBRS achieved in terms of cases successfully resolved?

- The mysteries of the application of the eligibility criteria

- The problems with Boundary and Concessionary Cases

- Why have there been so many resignations?

- An email trail that shows all is not well

- Has the BBRS handled evidence of criminality in the correct manner?

- The way forward:

- Why giving an expanded remit to the Financial Ombudsman Service would be a disaster; and why the Banks prefer that option

- The merits of independent tribunals

Are there any topics that you believe should be added to our response?

Here's the programme so far...

Andy Agathangelou

Founder, Transparency Task Force; Chair, Secretariat Committee, APPG on Personal Banking and Fairer Financial Services; Chair of the Violation Tracker UK Advisory Board

![]()